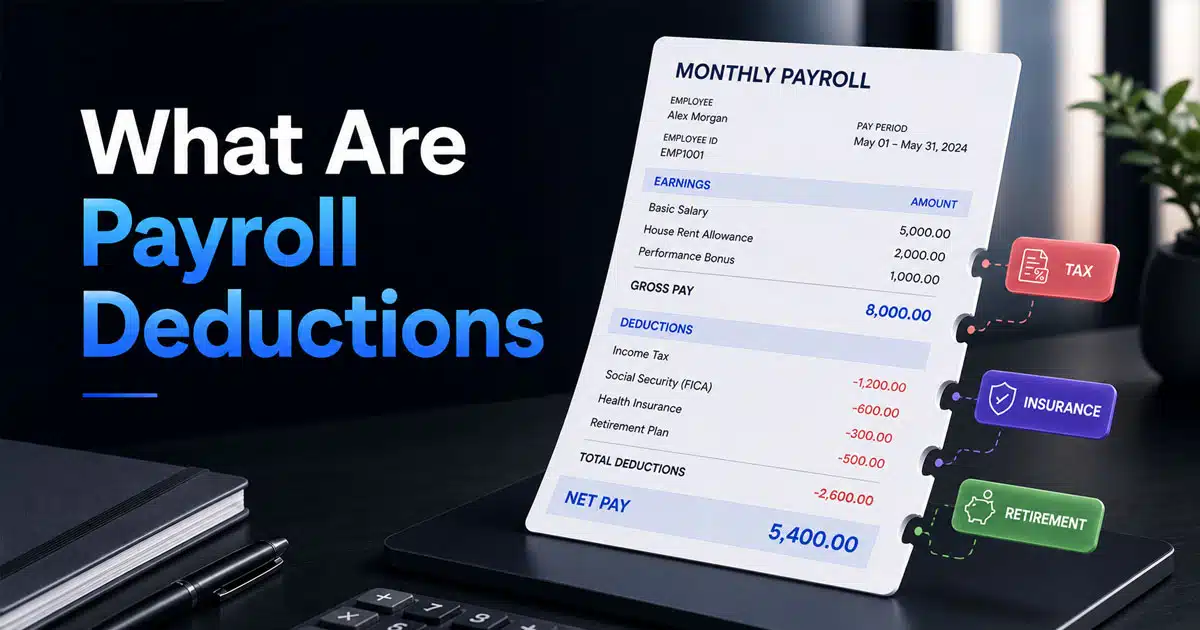

Every payslip tells the same story: gross pay enters at the top, deductions chip away in the middle, and net pay emerges at the bottom. Understanding deductions is important for financial planning and maximizing tax benefits for both employers and employees. Payroll deductions are specific amounts withheld from gross pay to cover taxes, benefits, and other financial obligations. These include income tax, National Insurance or FICA taxes, workplace pensions, health insurance, and wage garnishments where applicable.

The rules governing these withholdings come from tax authorities such as HMRC in the UK or the IRS in the US, alongside employee benefit agreements. Whether your payroll runs weekly, fortnightly, or monthly, accuracy is critical for compliance and employee trust. This article walks through how payroll deductions work, the common types you will encounter, step-by-step calculation methods, and how Payrun supports efficient payroll processing for growing businesses.

What Are Payroll Deductions

Payroll deductions are specific amounts withheld from an employee’s earnings each pay period before net pay is issued. Every time payroll runs, these deductions transform total compensation into the actual amount deposited into an employee’s bank account.

The distinction between gross pay and net pay sits at the heart of this process. Gross pay represents total earnings, including base salary, overtime calculated at 1.5 times the regular rate under FLSA rules, bonuses, and commissions. Net pay is what remains after all deductions have been subtracted, often called take-home pay.

Deductions are broadly categorized as mandatory or voluntary. Mandatory payroll deductions are required by law, including federal income tax, state income tax, and court-ordered wage garnishments. Voluntary deductions employees choose include contributions to retirement savings plans, health insurance premiums, and charitable donations.

Consider an employee earning 5,000 dollars gross monthly. After a $ 400 pre-tax pension contribution, $ 550 in federal tax withholding, $ 352 in FICA taxes, $ 200 in state tax, and $ 50 in union dues, the resulting net pay comes to approximately $ 3,448. This example illustrates how payroll deductions work to convert gross earnings into the final amount on the employee’s paycheck.

Types Of Payroll Deductions

Payroll deductions fall into structured categories based on tax treatment, legal requirements, and employee choices. Clear classification helps payroll teams apply correct rules, ensure compliance, and maintain accurate salary processing across every pay cycle.

Pre Tax Deductions

Pre tax deductions reduce an employee’s taxable income before income taxes are calculated. Common examples include health insurance premiums, retirement contributions, and certain commuter benefits. Since these amounts are deducted first, employees benefit from lower taxable wages and potentially reduced overall tax liability.

Employers must ensure each benefit qualifies under applicable tax laws. Incorrect classification can lead to compliance issues and reporting errors. Proper setup within payroll systems ensures accurate calculations and consistent application across all employees.

Post Tax Deductions

Post tax deductions are taken after all required taxes have been applied. These include items like wage garnishments, union dues, and voluntary deductions such as charitable contributions or life insurance premiums not eligible for pre tax treatment.

Unlike pre tax deductions, these do not reduce taxable income. Payroll teams must ensure correct sequencing so deductions apply after taxes. Clear documentation and employee authorization are essential to avoid disputes and ensure transparency in salary breakdowns.

Statutory Deductions

Statutory deductions are mandatory and required by law. These include income tax withholding, social security contributions, and other government-mandated payments depending on jurisdiction. Employers are responsible for calculating, withholding, and remitting these amounts accurately.

Failure to comply with statutory requirements can result in penalties, audits, and legal complications. Automated payroll compliance software helps ensure rates and thresholds remain updated, reducing risks tied to manual errors and outdated configurations.

Voluntary Deductions

Voluntary deductions are authorized by employees and typically relate to benefits or personal contributions. Examples include retirement savings plans, additional insurance coverage, and wellness program fees. These deductions depend on employee enrollment and consent.

Proper approval workflows and documentation are critical. Payroll teams must track changes, ensure accurate deductions each cycle, and maintain records for compliance and audit purposes. Clear communication helps employees understand how these deductions impact their take-home pay.

Mandatory Payroll Deductions And Legal Requirements

Mandatory payroll deductions are amounts employers must withhold from employee paychecks by law, including federal income tax, FICA taxes covering Social Security and Medicare, state income tax where applicable, and wage garnishments when a valid order is in place. These withholdings fund government programs and satisfy legal obligations regardless of employee preferences.

Tax related mandatory items differ from court ordered deductions. Income taxes and payroll taxes flow to government agencies based on applicable tax laws and income tax brackets. Court ordered deductions like child support payments or tax levies go directly to specified recipients or agencies following legal directives.

Income Tax Withholding

Employers withhold income tax each pay period based on information employees provide. The amount withheld for payroll deductions is influenced by the employee’s W-4 form, state and local tax laws, and any court orders that may apply. Federal income tax is withheld from employee paychecks based on progressive tax brackets, which range from 10% to 37%, and the amount withheld depends on the employee’s W-4 form and filing status. In the UK, tax codes from HMRC starter checklists determine withholding rates.

Federal income tax withholding must be updated when employees experience status changes such as marriage, new dependents, or changes in residency. The IRS publishes guidance in Publication 15-T with percentage methods and wage bracket tables for calculating correct withholdings based on pay frequency and filing status.

Errors in income tax withholding lead to underpayment notices at year end or larger than expected refunds, affecting employee satisfaction and employer compliance obligations.

Social Security, Medicare, And National Insurance Contributions

FICA taxes, which fund Social Security and Medicare, require employers to withhold 6.2% for Social Security and 1.45% for Medicare from each employee’s paycheck, and employers are legally obligated to match these amounts. The federal insurance contributions act establishes these rates, creating a combined 15.3 percent funding mechanism split between employee and employer.

An additional 0.9 percent Medicare tax applies on wages exceeding 200,000 dollars for single filers, deducted only from employee wages deducted with no employer match required. The Social Security wage base for 2024 stands at 168,600 dollars, with projections reaching 176,100 dollars by 2026 according to SSA trustees reports.

For UK employers, Class 1 National Insurance contributions apply at 8 percent on earnings between the primary threshold of approximately 12,570 pounds and the upper earnings limit of 50,270 pounds. Employers pay 13.8 percent above the secondary threshold of 9,100 pounds for the 2024 to 2025 tax year.

State, Local, And Regional Payroll Taxes

State and local income taxes add complexity depending on jurisdiction. Seven US states impose no income tax on wages, while others like California apply progressive brackets ranging from 1 to 13.3 percent. Some cities including Portland add local taxes up to 3 percent that must appear as separate lines on payslips.

Remote work patterns in 2026 require careful attention to multi state compliance. Employers must determine which jurisdiction rules apply based on where the employee works and sometimes where they live. New York’s convenience of employer doctrine, for example, taxes telecommuters even when working from other states.

Payrun can hold different rules per location, reducing manual tracking for employers managing federal state and local tax obligations across multiple jurisdictions, especially when using payroll processing software at scale.

Wage Garnishments And Court Ordered Deductions

Wage garnishments are mandatory deductions resulting from a court order or governmental agency that typically apply to a specific employee, often used to pay off debts such as unpaid taxes, defaulted student loans, alimony, or child support. These involuntary deductions follow strict procedures outlined in the garnishment paperwork.

The Consumer Credit Protection Act limits how much of an employee’s wages can be garnished per week and protects employees from being fired due to a single garnishment for any one debt. General creditor garnishments are capped at 25 percent of disposable earnings, while child support can reach 50 to 65 percent depending on circumstances.

Garnishment amounts are calculated from disposable earnings after legally required deductions have been taken, and the priority between multiple garnishments depends on the type of order and applicable federal and state law. Child support takes precedence over general creditors, followed by tax levies and bankruptcy orders.

Failing to remit garnished amounts makes the employer liable for arrears and possible penalties.

Employer Reporting And Recordkeeping Duties

Employers must report payroll tax deductions on periodic forms including quarterly Form 941 in the US and annual W-2 summaries by January 31 with electronic filing required when submitting 10 or more forms. These tax documents detail federal and state taxes withheld alongside employee wages.

In the UK, Real Time Information submissions go to HMRC on or before each payday, capturing PAYE, National Insurance, and student loan deductions. This reporting cadence ensures government agencies receive accurate data throughout the year rather than in a single annual filing.

Employers should retain employee payroll records, deduction authorizations, and court orders for three to six years depending on jurisdiction requirements. Modern systems like Payrun store digital records and support audit ready payroll reporting for authorities, reducing compliance risk from poor documentation.

Voluntary Payroll Deductions And Employee Benefits

Voluntary payroll deductions are optional amounts that employees can choose to have subtracted from their paychecks for various benefits, accounts, or services they’ve chosen to participate in. These elections typically occur during onboarding or annual enrollment periods.

Common types of voluntary payroll deductions include health insurance premiums, retirement contributions, and union dues, which can be taken either on a pretax or post-tax basis depending on the specific benefit type.

Health, Dental, And Vision Insurance Premiums

Many employers offer group medical, dental, and vision plans where employees pay part of the premium through payroll deductions. Health insurance premiums averaged 1,500 dollars monthly for employee share of family coverage according to 2024 Kaiser survey data.

In most arrangements, insurance premiums are deducted before income tax under Section 125 cafeteria plans, reducing taxable wages and total federal tax owed. This pre tax treatment provides immediate tax relief each pay period rather than requiring employees to claim deductions on annual returns.

Employees normally can change elections during open enrollment or after qualifying life events. A monthly premium split might show 400 dollars deducted from the employee’s pay with the employer covering the remaining 1,100 dollars of total family coverage costs.

Pension Schemes And Retirement Contributions

Common workplace retirement plans include UK automatic enrollment pensions and US 401(k) arrangements. Pre-tax deductions are taken from an employee’s paycheck before taxes are withheld, which can lower their taxable income and overall tax liability. For 2025, 401(k) contribution limits reach 23,000 dollars annually with additional catch up contributions of 7,500 dollars for those over 50.

Post-tax deductions are taken after all required taxes have been withheld and do not reduce the employee’s taxable income; examples include Roth IRA contributions and wage garnishments. Roth options defer tax benefits to withdrawal rather than providing current year savings.

UK auto enrollment requires minimum 8 percent total contributions split between 3 percent employer and 5 percent employee above the earnings trigger of 520 pounds quarterly. Many US employers offer matching contributions, commonly 100 percent on the first 3 percent deferred plus 50 percent on the next 2 percent, increasing the value of employee contributions significantly.

Flexible Spending Accounts And Health Savings Accounts

FSAs and HSAs allow employees in eligible health plans to set aside pre tax funds for qualified medical expenses or dependent care costs. FSA limits reach approximately 3,200 dollars for medical and 5,000 dollars for dependent care annually based on recent IRS guidance.

FSAs follow a use it or lose it rule within the plan year, though 2025 rules allow 610 dollar carryover or 2.5 month grace periods. This creates planning considerations for employees estimating annual healthcare spending.

HSAs tied to high deductible health plans offer contribution limits of 4,150 dollars for individuals and 8,300 dollars for families in 2025, plus 1,000 dollar catch up contributions for those 55 and older. Unlike FSAs, HSA balances roll over indefinitely, creating a triple tax advantaged long term savings vehicle. Average HSA balances reach 5,000 dollars after five years according to EBRI data.

Life, Disability, And Other Insurance Cover

Group term life insurance up to 50,000 dollars coverage qualifies as a tax advantaged benefit with no taxable benefits added to employee wages. Life insurance coverage above that threshold creates taxable imputed income calculated using IRS Table I rates and added to W-2 box 12.

Disability insurance premiums can be handled pre tax or post tax, with important implications. Pre tax premiums mean taxable benefits when paid, while post tax premiums result in tax free benefit payments during disability.

Other optional coverages including critical illness and income protection typically process as common post tax deductions. Clear employee communications about tax effects help staff make informed decisions during enrollment.

Union Dues, Charitable Giving, And Other Voluntary Deductions

Union dues are typically post tax deductions required under collective bargaining agreements, with amounts averaging 40 dollars monthly per BLS data. These amounts are set by the union rather than employer policy.

Employees may authorize voluntary charitable donations through payroll giving programs. UK approved schemes provide tax relief at source, while US programs may require employees to claim deductions on annual returns.

Additional voluntary deductions include share purchase plans, education savings contributions, and commuter benefits. Employers must track each authorization carefully and stop or change deductions promptly when employees request modifications within policy rules.

Pre Tax Versus Post Tax Deductions

The timing of a deduction relative to tax calculations determines whether it qualifies as pre tax or post tax. Pretax deductions are taken from an employee’s paycheck before any taxes are withheld, reducing taxable income and the amount owed to the government.

How Pre Tax Deductions Reduce Taxable Income

Pre tax deductions subtract from gross pay before tax calculations, lowering the base used for income tax and sometimes Social Security and Medicare. Common examples of pretax deductions include health insurance premiums, retirement contributions, and flexible spending accounts, which can lower both employee and employer tax liabilities.

Consider an employee with 5,000 dollars monthly gross who contributes 500 dollars pre tax to a 401(k). The employee’s taxable income drops to 4,500 dollars, saving approximately 110 dollars in federal tax at a 22 percent marginal rate. This creates immediate value compared to equivalent post tax savings.

Some pre tax benefits reduce only income tax while others reduce taxable income for both income tax and payroll taxes. Qualified retirement contributions typically reduce both, while Section 125 health premiums remain FICA taxable despite reducing income tax.

When Post Tax Deductions Are Used

Post-tax deductions can include contributions to Roth IRAs, wage garnishments, and union dues, which do not reduce taxable income but may offer other benefits. Roth contributions, for example, grow tax free and provide tax free withdrawals in retirement.

Typical post tax items processed through payroll include union dues, charitable contributions through standard payroll giving, life insurance premiums above the 50,000 dollar threshold, and most wage garnishments ordered by courts or government agencies.

These deductions do not change current year less income tax calculations, though they may offer advantages like tax free growth or immediate debt satisfaction. An employee choosing between pre tax 401(k) and Roth 401(k) contributions must weigh current tax savings against future tax free access.

Ordering Of Deductions Within The Payroll Cycle

Deductions are typically processed every pay period in a specific sequence: gross pay first, then pre tax deductions, followed by tax calculations, and finally post tax items and garnishments. This ordering ensures compliance with regulations defining how disposable earnings are calculated for garnishment purposes.

A typical sequence begins with 5,000 dollars gross pay. Pre tax deductions of 400 dollars for pension and 200 dollars for health insurance reduce taxable wages to 4,400 dollars. Federal tax of 500 dollars and FICA of 370 dollars are calculated on appropriate bases. Post tax union dues of 50 dollars and a garnishment of 100 dollars complete the cycle, leaving net pay of 4,380 dollars.

Changing this order incorrectly leads to underpaid tax or non compliance with garnishment limits.

Impact On Employer Paid Taxes And Costs

Some pre tax deductions lower employer paid taxes alongside employee savings. Employer FICA matching is calculated on wages after certain pre tax contributions, meaning lower employer paid taxes when employees maximize qualified retirement deferrals.

This can make offering pre tax benefits more cost efficient than equivalent salary increases. An employer with 100 employees each deferring 5,000 dollars annually to 401(k) plans saves approximately 38,250 dollars in employer FICA contributions compared to paying that amount as salary.

Post tax deductions generally do not reduce employer tax costs but may still support retention and engagement through valuable benefit offerings.

Common Compliance Pitfalls With Pre And Post Tax Rules

Typical mistakes include treating ineligible benefits as pre tax or failing to stop pretax deductions when employees become ineligible due to status changes. A 2023 SHRM study found 22 percent of payroll errors stem from outdated tax tables or incorrect deduction classifications.

Incorrect classification leads to tax penalties, corrected filings using forms like 941-X, and amended employee tax statements creating administrative burden and potential employee dissatisfaction.

Cross border employees and remote workers often trigger errors when rules differ by jurisdiction. Employers should document benefit plan rules carefully and configure payroll software before launching new schemes, with regular audits catching issues before they compound.

How Payroll Deductions Work In Practice

Calculating payroll deductions involves converting gross pay to net pay by subtracting various deductions, including taxes and benefits, from the total earnings. The process relies on accurate employee data, current tax rules, and correctly configured benefit selections.

Collecting Employee And Benefit Information

The process starts with collecting tax forms such as W-4 equivalents, starter declarations, national insurance numbers, and bank details. Employers can choose to calculate payroll deductions manually or automate the process using payroll software, which helps reduce errors and ensures compliance with tax laws.

HR or onboarding systems capture benefit elections, pension opt ins, and authorizations for voluntary deductions during employee setup. Court orders and agency notices for garnishments must be recorded with effective dates and reference numbers for accurate processing.

Keeping records updated when employees move, change hours, or change marital status prevents incorrect payroll deductions from affecting multiple pay periods.

Step By Step Flow From Gross Pay To Net Pay

The chronological flow begins with calculating gross earnings from base salary, overtime, shift premiums, commissions, and bonuses for the pay period. Pre tax deductions are subtracted next, reducing the amount subject to income tax withholding.

Tax calculations follow using appropriate rates for federal tax, state taxes, and local taxes based on the employee’s filing status and jurisdiction. FICA taxes calculate separately based on Social Security and Medicare requirements.

Post tax deductions and garnishments are subtracted last, with the final result representing net pay ready for payment and payslip generation.

Worked Example For A Single Monthly Pay Period

An employee earns 4,500 dollars gross monthly in 2026. Pre tax deductions include 300 dollars pension and 150 dollars health insurance, reducing taxable income to 4,050 dollars.

Federal income tax at an effective 18 percent rate comes to approximately 729 dollars. FICA taxes total 344 dollars calculated as 6.2 percent for Social Security and 1.45 percent for Medicare on the full 4,500 dollar gross. State income tax adds 180 dollars in a mid range state.

A post tax charitable donation of 25 dollars brings the final calculation. Net pay equals 4,500 minus 450 pre tax deductions minus 1,253 in total taxes minus 25 post tax, resulting in 2,772 dollars deposited to the employee’s bank account.

Understanding Payslips And Deduction Codes

Payslips show itemized lines for each type of earning and deduction, helping employees verify amounts. Typical codes include FED for federal tax, FICA-EE for employee FICA contributions, 401K for retirement contributions, and HLTH for health insurance premiums.

Many employers now provide digital payslips accessible via secure portals or apps, reducing paper costs while improving employee access. Year to date totals help employees track cumulative earnings and withholdings throughout the tax year.

Providing a short guide explaining deduction codes reduces employee support queries and builds confidence in payroll accuracy.

Handling Cross Border And Remote Employee Deductions

Modern work patterns often place employees in one jurisdiction while working for employers in another. Payroll deductions must follow local rules for tax residency, double tax treaties, and social security totalization agreements preventing dual taxation.

US totalization agreements with approximately 30 countries prevent dual Social Security taxation for expats, though state income tax sourcing rules still apply. A 2023 Deloitte survey found 15 percent of US companies faced new state filing requirements due to remote work arrangements.

Payrun supports multi location payroll workflows for growing teams, helping employers manage varying rules across jurisdictions without manual tracking for each employee location.

Common Payroll Deduction Mistakes And How To Avoid Them

Even experienced payroll teams make errors that lead to underpaid employees, overpaid taxes, and compliance penalties. A proactive approach to common payroll mistakes businesses must avoid prevents most issues before they affect payroll processing accuracy.

Misclassifying Workers And Applying Wrong Rules

Treating employees as independent contractors or vice versa leads to incorrect withholding and potential back taxes averaging 10,000 dollars per worker in IRS audit assessments. Status determination forms and official guidance help clarify worker classification before onboarding. Payrun setup differentiates clearly between employee and contractor records, enforcing correct deduction logic for each worker type and supporting robust employee vs contractor classification decisions.

Clear classification also supports long term compliance and reduces disputes. Payroll teams gain better visibility into tax obligations, while businesses avoid penalties tied to incorrect reporting and deduction errors.

Regular payroll audits help verify that classifications, deductions, and tax treatments remain accurate over time.

Using Outdated Tax Rates Or Thresholds

Tax authorities update rates, thresholds, and contribution limits annually. Failing to update payroll systems leads to under or over withholding requiring back adjustments and corrected forms throughout the tax year. Cloud payroll automation software solutions ensure current rules are applied as soon as updates release, eliminating manual rate updates.

Regular system checks ensure accuracy across payroll cycles. Automated updates reduce dependency on manual tracking, helping payroll teams maintain consistency and avoid costly corrections caused by outdated tax configurations.

Incorrect Handling Of Wage Garnishments

Errors occur when multiple garnishments exist or maximum limits on disposable earnings are not applied correctly. Employers must follow priority orders specified by law, with child support taking precedence over general creditors. Payrun helps track garnishment balances and ensures deductions stop automatically when orders are satisfied.

Accurate handling prevents legal complications and employee dissatisfaction. Clear tracking of balances and limits helps payroll teams maintain compliance while ensuring deductions remain fair and within statutory requirements.

Applying Wrong Tax Treatment To Benefits

Common errors include treating taxable benefits as pre tax or failing to record imputed income for employer provided life insurance coverage above 50,000 dollars. Each benefit plan should have documented tax treatment reviewed before configuration. Payrun validation rules and payroll audit tools flag inconsistencies in benefit setups before payroll runs process.

Proper configuration within dedicated payroll compliance software ensures benefits align with tax laws and reporting standards. Payroll teams reduce errors and maintain accurate records, helping organizations avoid penalties and improve financial transparency.

Lack Of Documentation, Audit Trails, And Approvals

Missing authorizations for voluntary deductions or absent copies of garnishment orders create risk during audits. Payroll changes should follow approval workflows with changes logged by user and timestamp. Payrun provides change histories and centralized document storage linked to employee profiles, supporting compliance requirements.

Structured documentation of employee payroll records strengthens audit readiness and accountability. Clear approval processes and recorded changes help payroll teams track decisions, reduce errors, and maintain compliance across all deduction activities.

How Payrun Helps You Manage Payroll Deductions

Payrun automates tax and contribution calculations for each pay period using current 2026 rates and thresholds across UK and multi jurisdiction payrolls, delivering the core automated payroll software features and benefits discussed earlier. The platform applies federal and state taxes, National Insurance, pension contributions, and benefit deductions consistently without manual recalculation.

Employers configure mandatory and voluntary deduction rules once, then apply them across all employees and locations. Digital employee self service allows staff to view digital payslips, review deduction histories, and request certain changes online without HR intervention.

Reporting and exports from payroll automation software support tax filings, garnishment remittances, and benefit provider reconciliation. Real Time Information submissions to HMRC process automatically, with audit trails maintaining immutable logs for compliance reviews.

Explore a Payrun demo to see how automated deduction calculations simplify your payroll processing and help your team manage deductions with confidence.

Frequently Asked Questions

Can Employees Change Their Voluntary Payroll Deductions At Any Time

Changes to voluntary deductions typically follow company policy and benefit provider rules, often limited to open enrollment periods or qualifying life events such as marriage or birth of a child. Some deductions like pension contributions within statutory ranges may be changed more frequently subject to scheme rules. Employees should contact HR or use self service tools in systems like Payrun to request changes, which take effect from a future payroll date.

What Happens If Payroll Deductions Would Reduce Pay Below Minimum Wage

Many jurisdictions restrict certain deductions if they would take an employee’s pay below the applicable minimum wage for hours worked. Mandatory taxes usually still apply, but optional deductions such as uniform fees may not legally reduce pay beneath the threshold. Employers should configure payroll rules so voluntary deductions are capped or skipped when they risk breaching minimum wage protections under FLSA section 6.

How Are Payroll Deductions Handled On Final Paychecks

When an employee leaves, employers must still withhold all applicable taxes and authorized deductions on the final paycheck. Some benefits like health coverage stop at termination dates, while garnishments apply until pay stops or orders are satisfied. Employers should follow local rules on timing of final pay, with 22 states requiring immediate payment, and provide clear final payslips itemizing all deductions.

How Can Payroll Deduction Errors Be Corrected In Later Periods

If an error is discovered, employers typically adjust in the next payroll run by adding or subtracting amounts and correcting tax calculations. Larger or older errors may require amended tax filings using Form 941-X and corrected employee tax statements. Payroll systems like Payrun provide adjustment tools and audit logs documenting why corrections were made.

Which Year End Forms Show Payroll Deductions To Employees

In the US, employees receive W-2 forms each January summarizing taxable wages and key takeaways payroll deductions for the prior calendar year, with box 1 showing wages after pre tax deductions and box 2 showing federal unemployment tax withheld amounts. UK year end data appears in P60 and P45 forms showing pay and tax totals including statutory deductions. Employees should compare these forms to payslips when completing personal tax returns.