Payroll tax rules have grown increasingly complex across Australia, the United States, and other major markets through 2025 and 2026. The Australian Taxation Office continues refining Single Touch Payroll Phase 2 requirements, while the Internal Revenue Service has intensified its audit focus on employment tax compliance and remote work classifications. Small and mid-sized employers face disproportionate exposure to these pressures because they often lack dedicated compliance teams, relying instead on manual processes or outdated systems.

Understanding payroll taxes is essential because these obligations differ from routine payroll errors. They involve statutory withholdings, employer liabilities, and filing deadlines that carry serious consequences including penalties, interest, back taxes, and director liability. Research shows that 33% of employers make payroll errors annually, leading to significant penalties and interest charges.

This article examines seven common payroll tax mistakes, explains how to recognise them early, and provides practical prevention steps. Payrun, a modern payroll platform, helps address many of these issues through automation and compliance tools.

What Is Payroll Tax Compliance

Payroll tax compliance represents the complete cycle of calculating employee-related taxes based on gross wages, withholding appropriate amounts from each paycheck, reporting totals to tax authorities via mandated tax forms, and remitting funds by strict deadlines to national, state and local governments. This encompasses federal income tax withholding, social insurance contributions such as PAYG in Australia or FICA taxes in the United States, employer obligations like federal unemployment tax (FUTA) or state payroll taxes where applicable, and contributions including superannuation or Social Security.

Compliance also requires registration in every jurisdiction where employees work, correct treatment of taxable fringe benefits under ATO FBT rules or IRS Section 132 exclusions, and accurate end-of-year reporting through payment summaries, W 2s, 1099 forms, or STP finalisations. The process demands attention to local tax requirements, state and local regulations, and federal state and local obligations simultaneously. Failing to maintain this compliance cycle creates exposure to employment tax errors and regulatory action.

7 Common Payroll Tax Mistakes

The following sections examine seven specific tax mistakes frequently observed in small businesses and mid-sized organisations across different industries from 2024 through 2026. Each subsection outlines how these common payroll errors typically arise, their financial and legal impact, and practical methods to prevent or correct them. Understanding these patterns helps business owners and payroll teams implement stronger controls before problems escalate into expensive liabilities.

1. Misclassifying Employees And Independent Contractors

Misclassifying workers as independent contractors instead of employees is one of the most common payroll tax mistakes, which can lead to significant tax fines and penalties. Businesses sometimes classify workers as contractors to sidestep PAYG withholding, superannuation contributions, or FICA obligations in the short term. However, audits frequently reclassify these workers, triggering several years of back-tax assessments.

Employers must evaluate the relationship with workers based on control over work, financial arrangements, and the nature of activities performed to ensure correct classification under tax law. Practical factors include whether the business provides equipment, sets work schedules, reimburses expenses, or integrates the worker into daily operations.

Consider a scenario where a business classifies several freelance sales representatives as contractors while providing them laptops, sales scripts, and mandatory training. An audit in 2025 could result in unpaid employer payroll taxes, interest, and penalties. Improperly classifying employees as independent contractors can expose businesses to penalties of up to 100% of both the employee and employer portions of FICA taxes.

Prevention requires reviewing all contractor relationships annually, documenting classification decisions with clear contracts, and using available tax authority tools. Proper worker classification is vital to avoid heavy penalties associated with misclassifying employees, and businesses can benefit from a structured employee vs contractor classification guide for payroll compliance. Payrun separates contractor payments from employee payroll processing, though legal responsibility for classification remains with the employer.

2. Missing Payroll Tax Deposit Deadlines

Failing to meet payroll tax deposit deadlines can result in escalating penalties from the IRS, starting at 2% for deposits 1-5 days late and increasing to 15% for amounts unpaid more than 10 days after the first notice. This mistake topped IRS penalty assessments with 2.5 million notices issued in 2024, with small businesses hit hardest.

Employers must deposit both the employer and employee portions of Social Security and Medicare taxes on a set schedule, which may be monthly or semiweekly depending on total payroll tax liability. Deposit frequencies shift based on lookback periods, and small employers often miss changes when they cross payroll size thresholds without warning.

The IRS imposes escalating penalties for late payroll tax deposits, starting at 2% for deposits 1-5 days late and escalating to 15% for amounts still unpaid more than 10 days after the first IRS notice. A retailer missing semiweekly FICA deposits on a $200,000 liability could face $15,000 or more in penalties.

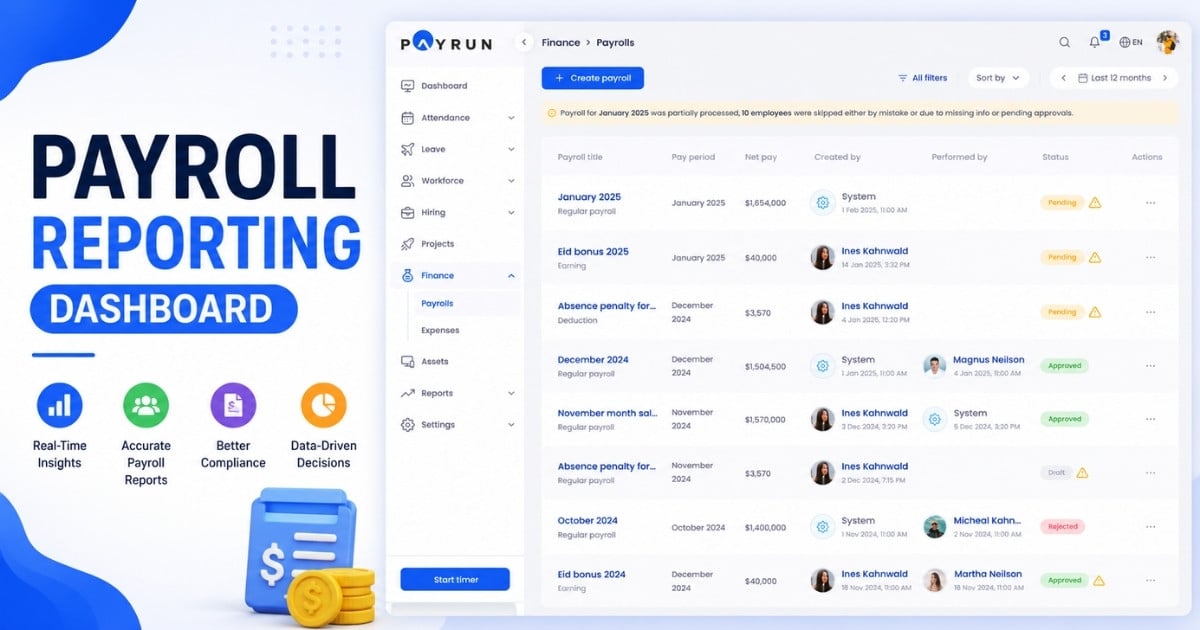

Controls include maintaining dedicated tax bank accounts, using automated EFT payments, and setting calendar reminders through payroll software rather than manual spreadsheets. Electronic tax deposits can automatically handle timely tax submissions to prevent penalties. Payrun generates deposit summaries and schedules, flagging payroll tax payments before due dates to help prevent these costly oversights, similar to broader payroll compliance software that automates calculations and multi-jurisdiction filing requirements.

3. Miscalculating Wage Bases And Taxable Wages

Wage bases cap certain taxes and reset annually. For 2026, the Social Security wage base limit stands at $176,100, while medicare tax applies without limit. The additional medicare tax of 0.9% applies on earnings exceeding $200,000. State unemployment insurance thresholds vary by jurisdiction, and Australian state payroll tax thresholds range from approximately AUD 1.2 million to AUD 1.8 million depending on the state.

Common payroll mistakes include continuing to withhold Social Security after the wage base limit is reached, creating overpayments that require refunds. Conversely, failing to withhold payroll taxes on bonuses, commissions, or back pay creates underpayments subject to penalties. Approximately 20% of audited firms experience these types of wage base calculation errors.

Failing to accurately calculate overtime can lead to violations of the Fair Labor Standards Act (FLSA). Similarly, misunderstanding wage and hour laws creates additional exposure under overtime pay requirements and minimum wage regulations.

Consider a manufacturer in 2026 that over-withholds Social Security by $10,000 on overtime payments while simultaneously underpaying state unemployment taxes by $5,000 due to stale tax tables. Prevention uses current IRS Publication 15 tables and year-to-date tracking per employee. Payrun automatically applies wage base limits and alerts users when manual overrides could create mismatches in taxable wages calculations, offering the same advantages highlighted in automated payroll software features and benefits.

4. Failing To Register In New States Or Jurisdictions

Many businesses fail to register for State Unemployment Tax Act (SUTA) accounts in every state where they have employees, including remote workers. Remote and hybrid work trends since 2020 have led to staff working across multiple states or regions, triggering registration requirements for unemployment insurance, local payroll taxes, and income tax withholding.

An e-commerce firm that hires a California remote worker in 2025 but continues withholding and reporting only in Texas creates serious compliance problems. This oversight can result in $20,000 or more in back taxes, 10% penalties, and potential double taxation complications. Non-registration also blocks unemployment taxes credits and delays access to state incentives.

Each state has specific thresholds for registration, typically triggered by $1,500 in first-quarter wages or employing even one worker in that jurisdiction. Local tax authorities may impose additional requirements in certain municipalities.

Prevention steps include tracking employee locations through hire reporting systems, consulting each state’s registration requirements immediately upon hiring, and setting up tax accounts before the first payroll runs. Payrun maintains separate tax profiles per location and supports multi-state payroll, ensuring withholding taxes and reporting are properly split where staff actually perform work, a growing necessity as payroll regulations evolve for growing companies in 2026.

5. Ignoring Changes In SUTA Or State Payroll Tax Rates

State unemployment insurance rates and state payroll tax rates update annually via mailed notices. Rates are experience-rated based on the employer’s industry, total wages subject to tax, and claims history. New employers typically start at approximately 2.7% nationally, while established businesses may see rates ranging from 0.1% to over 12% based on their experience.

Employers often misplace these rate notices or forget to update their payroll system, causing underpaid or overpaid contributions throughout the calendar year. The 2026 rates reflect 2025 claims experience, meaning changes can be significant.

A retailer using the prior year’s 2.1% SUTA rate throughout 2026 when the correct rate should be 3.4% could face an unexpected bill of $8,000 or more on $4 million in wages after state reconciliation. This creates cash flow strain and potential penalties for underpaying payroll taxes.

To avoid this mistake, capture rate notices immediately upon receipt, document where entries were made in the system, and verify the first few pay cycles each January or fiscal year start. Payrun enables easy updating of SUTA and regional payroll tax rates and produces reports showing the rate applied each pay period for audit and reconciliation purposes, which is especially useful for small firms following a detailed payroll compliance guide for small businesses.

6. Incorrectly Calculating Or Withholding Payroll Taxes

Miscalculations in withholding taxes often stem from outdated tax tables, incorrect employee declarations, or manual overrides on irregular payments. Employers must ensure that all employees fill out a Form W-4 for accurate tax withholding calculations. Similar requirements apply in Australia through TFN declarations.

Specific problem areas include applying incorrect rates to supplemental wages like bonuses, failing to calculate additional medicare tax on high earners, mishandling equity compensation like RSUs at vesting, and incorrectly taxing non-cash benefits such as company cars, allowances, or relocation packages under taxable fringe benefits rules.

Even minor per-pay under-withholding of $50 across 100 employees accumulates into a $24,000 annual tax liability requiring correction. Garnishments must be withheld and paid to the appropriate authority until a written release is received, adding another layer of complexity to each pay period.

Practical tips include locking down manual tax changes, requiring review of unusual payment types before processing payroll, and regularly reconciling total tax withheld to reported amounts. Payrun applies current tax rules and special tax treatments for bonuses, commissions, and other complex payments, significantly reducing manual calculation risk while ensuring compliance with personal income taxes requirements, functioning as robust payroll processing software for business payroll.

7. Filing Inaccurate Or Late Payroll Tax Forms

Accurate and timely filing of core payroll forms remains essential for tax compliance. Quarterly employment tax returns, annual reconciliation forms, and year-end employee statements must align with deposits and employee wages data. Errors on forms such as Form 941 or W-2 can trigger audits and rejected filings.

Form W-2s must be delivered to employees and submitted to the Social Security Administration by January 31st. Quarterly 941 filings are due by the end of the month following each quarter. Late 941 submissions incur 5% monthly penalties up to 25% of unpaid amounts.

Frequent mistakes include transposed figures, missing employee identifiers, mismatched totals between returns and payroll tax records, and submitting forms after filing deadlines. Approximately 30% of audit triggers involve transposed employer identification numbers or mismatched totals.

Controls include formal pre-filing reviews, using e-file where available (now accounting for 94% of IRS filing volume), and reconciling payroll records to tax forms every quarter rather than waiting until year-end. Payrun produces ready-to-file reports and electronic files for statutory reporting while providing clear audit trails for corrections when amendments become necessary, supporting more effective payroll audit strategies to ensure accuracy and compliance.

Legal And Financial Risks Of Payroll Tax Mistakes

Noncompliance with payroll tax requirements can lead to substantial legal and financial ramifications, including penalties, fines, and interest charges imposed by tax authorities. A seemingly small payroll tax oversight in 2024 can escalate into a multi-year problem costing thousands by 2026 after interest and penalties compound.

Direct financial consequences include civil penalties starting at 2% and escalating up to 15%, interest charges accruing at approximately 8% annually, disallowed deductions, and requirements to pay both the employee and employer portions of unpaid employment tax. These significant penalties create immediate cash flow pressure while diverting management attention from growth activities.

Impact On Cash Flow And Budgeting

Missing payroll tax deposit deadlines can lead to significant financial burdens due to penalties and interest charges that accumulate over time. A late $10,000 FICA deposit incurs approximately $500 in penalties plus $200 in monthly interest. Left unaddressed, this can double to $20,000 or more by the end of the following year.

For small businesses operating with thin 5-10% margins, these unexpected costs create serious liquidity problems. Missed deposits can force double payments in a single period when both the late amount and current liability come due simultaneously, creating a short-term cash squeeze that disrupts operations.

Proactive budgeting for payroll related taxes includes holding funds in a segregated account and forecasting liabilities based on projected employee wages for each quarter. Payrun reports help forecast upcoming payroll tax obligations, allowing finance teams to plan and avoid liquidity surprises.

Reputational Damage And Employee Trust

Payroll tax problems often surface when employees attempt to file their own income taxes and discover mismatches between their pay slips and official records. Incorrect W 2s or payment summaries force employees to amend their returns, creating delays in refunds averaging 8 weeks and causing significant employee dissatisfaction.

Ongoing common payroll errors erode trust in leadership and HR teams, increasing staff turnover and making it harder to attract new talent in competitive markets. Research indicates approximately 25% of turnover relates to payroll issues. These employment tax errors damage your reputation as a reliable employer.

When corrections are required, communicate transparently with affected staff, providing clear timelines and steps being taken to resolve issues. Strong, consistent use of compliant payroll systems demonstrates commitment to accuracy and fairness in how employees are paid and taxed.

Regulatory Scrutiny And Audits

Audits triggered by payroll tax violations can require extensive documentation and investigations, potentially leading to corporate limitations and loss of eligibility for government contracts. Repeated filing errors, frequent late deposits, or obvious discrepancies between reported wages and industry norms increase audit likelihood.

Inadequate record-keeping practices can complicate audits and expose organizations to risks, as incomplete or disorganized data makes it difficult to verify payments and track accruals. Audits typically involve requests for records going back several years, interviews with staff, and time spent compiling documentation instead of serving customers.

The IRS requires employers to keep payroll records for at least four years after the tax becomes due or is paid, while state requirements may vary, generally requiring records to be maintained for three to six years. Employers are legally required to maintain payroll tax records, including timesheets, payroll tax withholdings and deposits, copies of filed payroll forms, employee benefits and deduction records, and documentation for special types of compensation, for a minimum of four years.

Annual internal or external payroll audits help identify problems before regulators do. Payrun’s reporting and export capabilities make supplying comprehensive, well-organised data straightforward if an audit or review occurs.

How To Prevent Payroll Tax Mistakes Proactively

To avoid payroll errors, businesses must understand complex tax laws, stay compliant with federal and state requirements, and use tools or partners that support accurate, timely payroll processing. Proactive planning and precise data management are essential for ensuring accuracy in payroll tax processes to avoid penalties ranging from 2% to 15%.

Effective prevention combines strong processes, clear responsibilities, reliable technology, and periodic review rather than relying solely on any single element, echoing the core themes in guidance on payroll mistakes businesses must avoid in 2026.

Implementing A Payroll Compliance Calendar

Implementing a payroll compliance calendar can help businesses keep track of important deadlines for tax filings and payments, reducing the risk of penalties for late submissions. Build a detailed calendar for 2026 that includes all key dates: deposit deadlines, quarterly returns, annual reconciliations, and year-end employee statement due dates.

Critical dates include January 31st for W-2 delivery and Form 940 annual FUTA filing, April 30th for Q1 Form 941, and corresponding quarterly deadlines throughout the year. Incorporate reminders at least one week before each due date and assign clear ownership to specific people or roles, not generic departments.

Integration with digital tools such as shared calendars, project management systems, or Payrun notifications ensures deadlines remain visible to both finance and HR teams. Review the calendar periodically as rules change or as the business expands into new jurisdictions or different deposit frequencies under the payroll schedule, especially if you are still transitioning from Excel to payroll software and formalising processes.

Standardising Payroll Tax Procedures

Written procedures covering data collection, approval workflows, tax calculation checks, deposit authorisations, and filing steps for each payroll cycle create consistency and reduce errors. Document how to handle edge cases including bonuses, back pay adjustments, terminations, non exempt employee classifications, and retroactive pay rate changes.

Segregation of duties remains important where possible. Separate the person who prepares payroll from the one who approves tax payments to maintain appropriate controls.

A checklist used before finalising each payroll run should verify current tax rates, new hires, terminations, location changes, and compliance with payroll laws. Payrun workflows can reflect and reinforce these procedures, making consistent application straightforward every pay period and delivering many of the advantages of a modern payroll management system.

Training Staff On Current Payroll Tax Rules

Employers should regularly review their payroll systems to ensure they are updated with the latest tax rates and regulations, as outdated systems can lead to compliance issues. Payroll and HR staff must stay current with frequent regulatory changes including new thresholds, rates, reporting formats, and remote work rules.

Schedule at least annual training sessions, plus targeted refreshers when major changes take effect such as new tax year rules or updated reporting systems. Use official guidance from tax authorities, webinars, and professional advisors rather than relying only on informal sources.

Include real case studies or anonymised internal incidents in training to make risks and solutions concrete for staff. By configuring Payrun correctly and using its compliance resources, payroll teams can focus learning on understanding changes rather than manual recalculation of tax liability, building on the fundamentals outlined in a comprehensive guide to payroll processing for growing businesses.

Leveraging Automation And Payroll Software

Automating payroll and taxes significantly reduces manual data entry errors and helps ensure compliance with the latest tax rates and laws. Modern payroll software handles recurring calculations, applies updated tax tables, generates statutory reports, and helps schedule deposits with far fewer errors than manual spreadsheets, which carry approximately 40% error rates.

Automated payroll systems help companies avoid common payroll tax mistakes and maintain compliance with federal regulations. Automation does not remove the employer’s legal responsibility but significantly reduces risk of arithmetic errors, missed deadlines, and inconsistent treatment between employees.

Specific benefits include automatic calculation of superannuation or retirement contributions, real-time gross-to-net previews, and automated preparation of quarterly returns. Evaluate whether current tools keep pace with recent changes or whether migrating to a platform like Payrun would improve accuracy and efficiency in the payroll process by leveraging the benefits of payroll automation software for faster and accurate payroll processing and the broader capabilities described in this complete guide to payroll software features and automation.

Conducting Regular Payroll Reconciliations

Regular audits should be performed to match internal payroll records against bank debits and tax filings to identify discrepancies early. Reconciling payroll involves matching gross wages, taxable wages, and taxes withheld in the payroll system to amounts actually deposited and reported to local tax authorities and federal agencies.

Perform reconciliations monthly or at least quarterly, and always before filing statutory returns or issuing year-end employee statements. Common steps include checking totals by tax type, confirming deposit receipts, and reviewing any manual overrides or adjustments.

Maintain a reconciliation log documenting who performed checks, what issues were found, and how they were resolved for future audits. Payrun provides detailed reports exportable to accounting systems or spreadsheets, making documentation of these reconciliations straightforward.

How To Correct Payroll Tax Mistakes When They Happen

Even well-run payroll operations occasionally make errors. Prompt, structured corrections limit financial and reputational damage while demonstrating good faith to tax authorities.

Identifying And Assessing Payroll Tax Errors

Errors commonly surface through reconciliation discrepancies, employee questions, notices from the internal revenue service or other tax authorities, or internal audits. Initial assessment should determine which periods and employees are affected, the size of the variance, and whether underpayment, overpayment, or misreporting has occurred.

Prioritise time-sensitive issues, especially missed deposits or filing deadlines where penalties and interest continue to accrue until resolved. Compile a clear summary of findings for internal use and discussions with advisors or tax authorities.

Payrun’s history logs and detailed payroll reports help quickly identify when and where an error began, streamlining the assessment process and reducing response time, which is particularly valuable for startups adopting payroll software for startups and growing teams.

Using Amended Returns And Adjustment Forms

Many payroll tax violations are corrected by filing amended employment tax returns or adjustment forms specific to the relevant jurisdiction. Examples include correcting underreported wages or misclassified workers on prior quarterly returns using forms like the 941-X.

Deadlines and processes for amendments vary across jurisdictions. Some allow interest-free corrections if filed promptly, while others impose different limitation periods. Consult a qualified tax advisor when handling large or multi-year corrections to minimise penalties and meet documentation standards.

Payrun generates corrected payroll figures needed to support amended filings and maintains clear records of all changes for audit purposes.

Communicating With Employees About Corrections

Transparent communication matters when payroll tax corrections affect employee pay, tax slips, or refunds. This is especially important close to individual filing deadlines when employees rely on accurate documentation.

Provide written explanations stating what went wrong, how it has been fixed, and what employees must do, such as using corrected year-end documents. Offer a nominated contact point in HR or payroll to answer questions and reduce confusion.

Coordinate internal communication timing with actual filing of corrected forms to prevent mismatches between what employees receive and what authorities have on record. Payrun makes regenerating updated payslips and year-end summaries straightforward so employees receive accurate documentation promptly.

Learning From Mistakes To Improve Controls

Perform a brief root-cause analysis after each significant payroll tax mistake to determine whether the issue stemmed from process gaps, training deficiencies, outdated systems, or unclear responsibilities. Update written procedures, checklists, and training materials accordingly.

Track recurring themes across mistakes to identify systemic weaknesses. If issues consistently arise with new state registrations or bonus taxation, those areas require additional focus.

By combining strong internal controls with Payrun’s automation and reporting, businesses significantly reduce long-term exposure to employment tax errors and build more resilient payroll operations, especially when supported by modern cloud HR software for modern teams.

Final Discussion

Payroll tax errors rarely come from complexity alone; they often result from inconsistent processes, outdated knowledge, and a lack of regular audits. Missing deadlines, misclassifying employees, or applying incorrect tax rates can quickly lead to penalties and compliance risks. A proactive approach helps avoid these issues. Standardize payroll workflows, maintain accurate employee records, and stay updated with changing federal and state regulations.

Automation also reduces human error. Reliable payroll systems ensure calculations remain accurate and filings stay on schedule. Regular reviews of payroll data can uncover discrepancies before they escalate, and broader HR management platforms with innovative features can centralise these controls across payroll, leave, and expenses.

Avoiding common payroll tax mistakes is less about reacting to problems and more about building a structured, reliable process. With the right systems and discipline in place, businesses can maintain compliance, reduce risk, and ensure smooth payroll operations, particularly when using HR and payroll software for SaaS and software businesses that centralises data and workflows.

Frequently Asked Questions

How Often Should A Small Business Review Its Payroll Tax Settings

Review payroll tax settings at least quarterly and again at the start of every new tax year. Additional reviews are necessary whenever the business hires in a new state or jurisdiction, introduces new pay types like bonuses or equity compensation, or faces major legislative changes affecting tax regulations. Payrun helps confirm that all updates have been properly applied across the system, reflecting its broader role as your trustworthy partner in HR management.

What Should I Do If I Discover A Payroll Tax Error From A Prior Year

Quantify the error immediately, identify all affected periods and employees, and consult current rules or a tax advisor to determine the correct amendment process for self employment tax or employment taxes in those years. Act quickly, as some jurisdictions limit how long you have to correct returns or claim refunds. Interest on underpaid amounts continues accruing until paid, making prompt action financially beneficial.

How Can I Handle Payroll Taxes For Remote Employees Working Overseas

International remote workers often create both domestic and foreign payroll tax obligations, involving registration in the employee’s country and complex treaty considerations. Obtain specialist cross-border tax advice before hiring or converting staff to overseas remote roles. Use Payrun configurations aligned with that advice for accurate withholding and reporting that meets both employer and local tax requirements, and ensure overseas staff absences are tracked through robust leave management for remote teams.

Is It Safe To Rely Solely On My Payroll Provider For Tax Compliance

While a reliable provider or software significantly reduces risk, the employer remains legally responsible for correct tax calculation, deposits, and filings. Maintain oversight through regular report reviews, reconciliations, and confirmation that filings and missed payments have been addressed as scheduled. Never assume everything is handled automatically without verification.

When Should A Business Consider Outsourcing Payroll Tax To Specialists

Outsourcing or seeking specialist support is valuable when the organisation grows quickly, hires across multiple states or countries, or introduces complex compensation structures like equity or variable bonuses. Even when working with external experts, keeping payroll processing on a robust platform such as Payrun provides transparency, data control, and reliable day-to-day automation that supports both the employee and employer interests, as part of a broader all-in-one HR platform that streamlines core workforce processes.