Half of American workers couldn't cover a $1,000 emergency from savings, yet payday still sits two weeks away. That gap is exactly what earned wage access was built to close. So what is earned wage access, in plain terms? It lets employees pull a portion of already-earned wages before their scheduled payday, straight to a bank account, instead of waiting out the full pay cycle.

Also known as early wage access or on-demand pay, wage access works alongside existing payroll, not around it. Employers don't front any cash, and employees aren't taking on debt, just claiming earned wages they've already worked for. For a workforce living paycheck to paycheck, that shift changes how financial stress gets handled day to day, and this guide breaks down exactly how it works.

What Is Earned Wage Access

Earned wage access is a benefit that lets employees withdraw part of their pay before the end of the current pay period, based on hours already worked. Instead of waiting for payday, an employee requests funds through an earned wage access provider, which integrates directly with employer payroll systems to confirm what's actually been earned.

On payday, that amount is deducted automatically, so there's no separate repayment step. For workers facing a cash shortfall, using an EWA provider is often a cheaper alternative to overdraft fees or high-interest short-term loans.

Why Employees Are Turning To Earned Wage Access

The reasons aren't complicated. Pay arrives on a fixed schedule, but expenses don't. Between rigid pay cycles, thin savings, and predatory lending alternatives, earned wage access benefits have become less of a perk and more of a necessity for many workers.

Biweekly Or Monthly Pay Cycles

Most employees get paid every two weeks or once a month, a schedule set by payroll providers long before flexible spending needs became the norm. Unexpected expenses, a car repair, a medical bill, don't wait for that cycle to end. Earned wage access apps exist precisely because of this mismatch. Rather than changing how often payroll runs, wage access apps let employees draw against hours they've already worked, closing the gap between when money is earned and when it's actually available.

Workers' Savings Buffer Gap

Nearly half of American workers can't cover a $1,000 emergency without borrowing or falling behind on bills. Without a savings cushion, even a minor unexpected expense turns into a scramble. Earned wage access services fill that specific gap, giving employees a way to access funds they've already earned instead of turning to credit cards or family loans. It's not a replacement for savings, but it softens the blow when there isn't any.

Exploitative Payday Loan APRs

Predatory payday loans often carry annual percentage rates north of 300%, structured around short repayment windows and steep fees. Workers who don't qualify for traditional credit frequently have no other fast option. EWA services offer a meaningfully cheaper alternative, usually a flat fee or no fee at all, repaid through a simple payroll deduction rather than compounding interest. That difference alone is why so many employees now actively look for wage access benefits when comparing employers.

Financial Stress And Work Productivity

Money worries don't stay home when an employee clocks in. Surveys consistently show financial stress is a leading distraction at work, pulling focus away from tasks and increasing turnover risk. Offering earned wage access benefits gives employees one less thing to carry into their shift. When people aren't quietly calculating how to cover a bill until payday, they're simply more present, and more productive, on the job.

Rising Demand From Younger Workers

Younger employees, particularly Gen Z and Millennials, expect financial flexibility as a standard benefit, not an extra. Having grown up with instant banking apps and real-time notifications, waiting two weeks for money they've already earned feels outdated to them. This demographic shift is pushing adoption fast, and employers slow to offer wage access services may find themselves at a real disadvantage when competing for talent in tighter labor markets.

How Earned Wage Access Actually Works

The mechanics are simpler than most people expect. Earned wage access ewa isn't a loan process or a credit application; it's a direct link between hours worked and money already owed. Here's exactly how it functions, step by step.

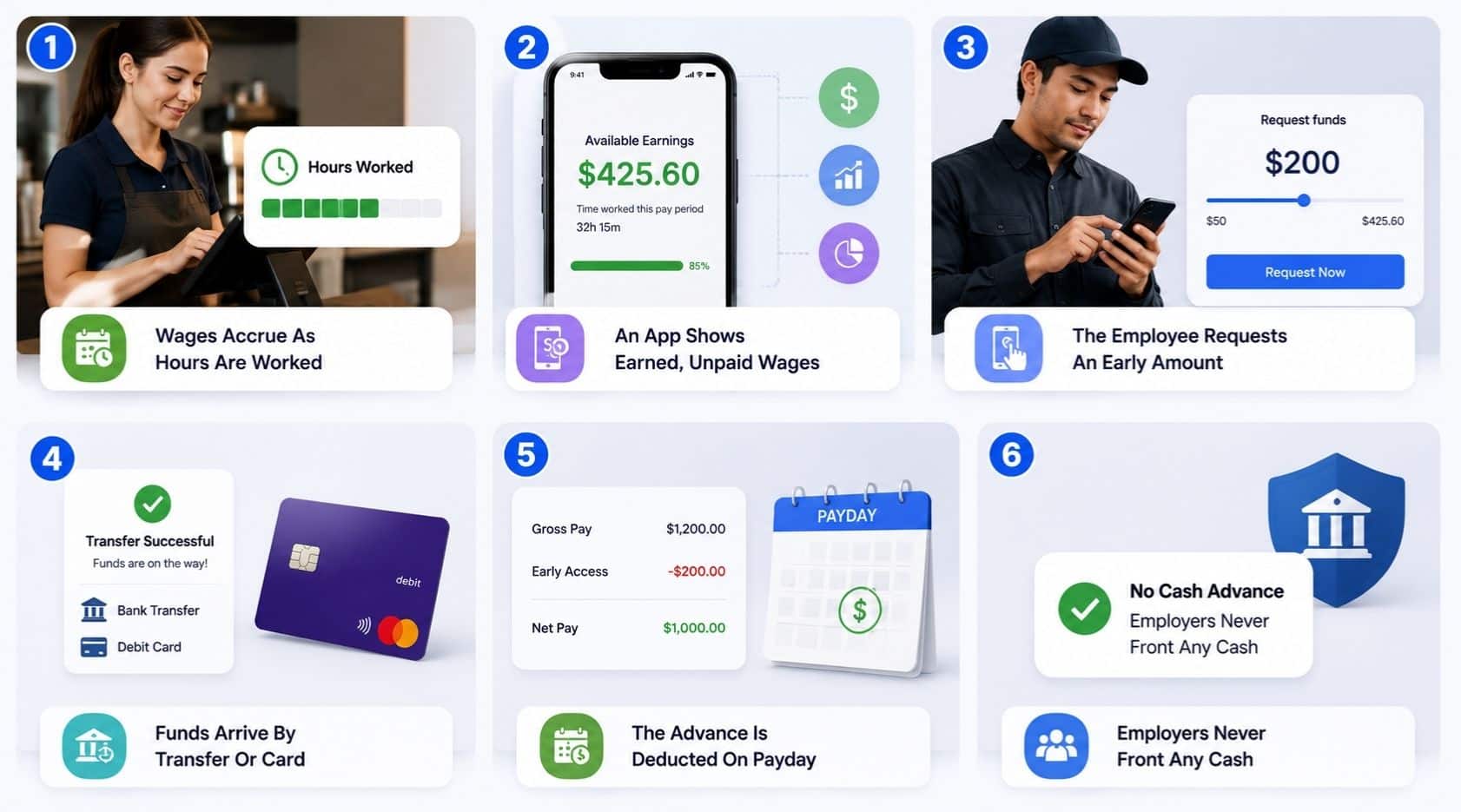

Wages Accrue As Hours Are Worked

Every shift an employee completes adds to a running total of earned but unpaid wages, tracked in real time through the employer's payroll or time-tracking system. This isn't an estimate or a projection, it's money the employee has already earned through actual hours logged, just not yet disbursed on the standard pay schedule. This accrual is the foundation the entire benefit rests on, and accurate employee time log reports make that foundation reliable. Without accurate, real-time tracking of hours and pay rates, there's no reliable number to offer early access against, which is why EWA depends so heavily on tight integration with payroll management systems rather than working as a standalone guess.

An App Shows Earned, Unpaid Wages

Once wages accrue, employees typically see the running total through a mobile app connected to the employer's system. This visibility is a core piece of most financial wellness tools and digital payslip software built into modern EWA platforms, since it gives employees a clear, constantly updated picture of what they've earned so far in the current pay period. Rather than waiting for a pay stub to find out, employees can check their balance whenever they want. This transparency also reduces guesswork; workers know exactly how much they can request without needing to call HR or estimate their own hours.

The Employee Requests An Early Amount

When a need comes up, employees access earned wages by submitting a request directly through the app, up to a set percentage of what's already accrued. Employer participation determines the exact limits here; some cap early access at 50% of earned wages, while others allow more flexible access depending on the provider and company policy. This request step is typically instant, with no approval process, credit check, or waiting period, since the employee is only accessing money that's already theirs, not applying for new credit.

Funds Arrive By Transfer Or Card

Once a request is approved, funds move quickly, often within minutes to a few hours. Employees can usually choose how they receive the money: direct deposit to a bank account, transfer to a linked debit card, or, in some cases, a prepaid card tied to the EWA provider. Faster options may involve a small fee, while standard transfers within one to three business days are often free. This flexible access to funds is what separates EWA from traditional pay cycles, giving employees control over timing without disrupting how the underlying payroll cash flow actually operates.

The Advance Is Deducted On Payday

When the regular pay date arrives, the amount already advanced is automatically subtracted from that paycheck, so employees receive the remaining balance as usual. There's no separate bill, no repayment schedule to track, and no risk of late fees since the deduction happens seamlessly within standard payroll processing. Some providers charge a flat fee per transaction; others use a monthly subscription fee model instead, but either way, the deduction itself is handled automatically without requiring any action from the employee.

Employers Never Front Any Cash

This is the detail that makes EWA an appealing employee benefit for businesses to offer. The earned wage access provider funds the early payment, not the employer, meaning company cash flow stays completely untouched, especially when paired with payroll processing software that keeps calculations and disbursements accurate. Employers essentially offer the benefit by enabling the integration, not by covering advances out of pocket. Research from the Financial Health Network and similar studies has pointed to this as one of the reasons EWA has scaled so quickly among employers who want to support financial wellness without taking on financial risk themselves.

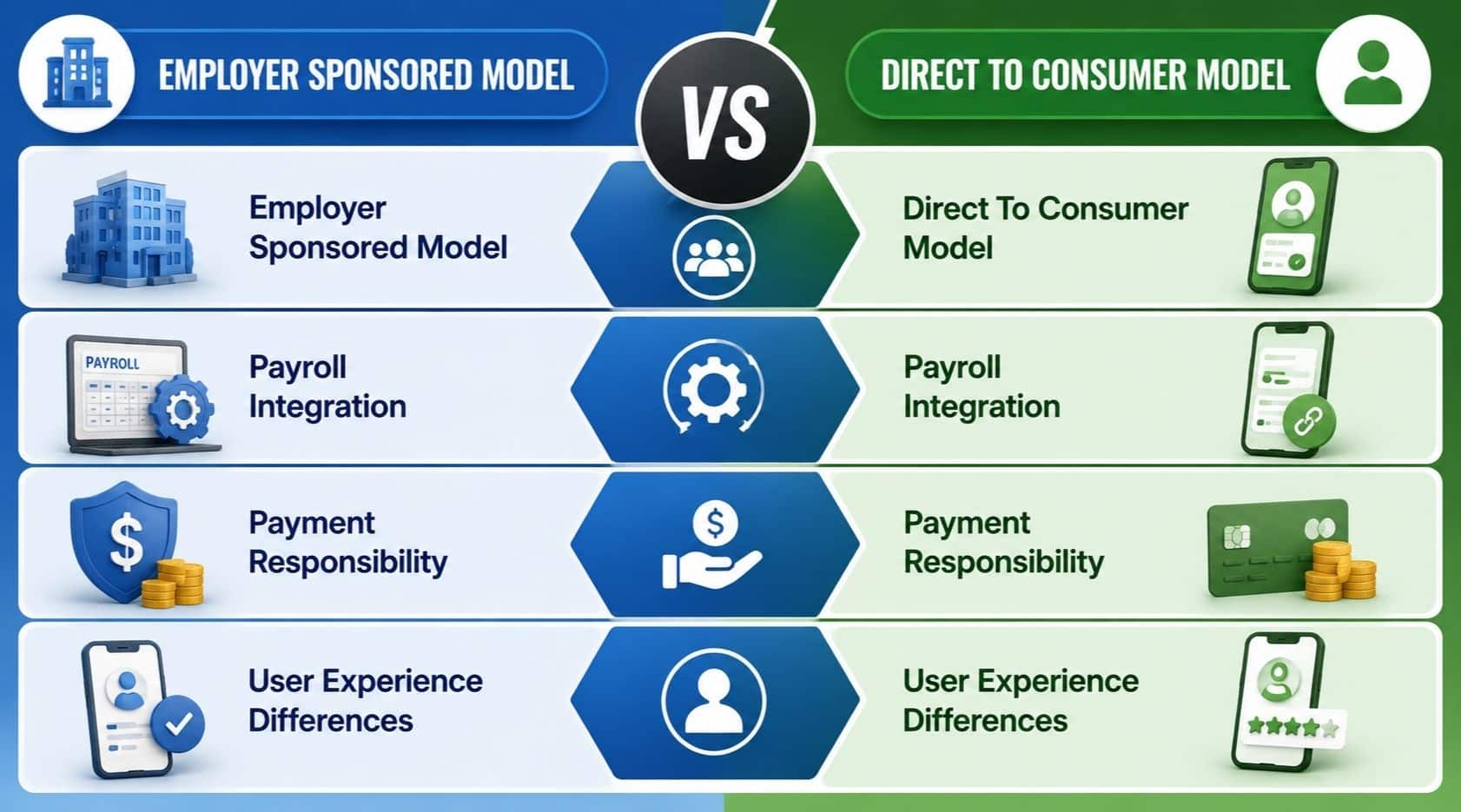

Employer Sponsored Vs Direct To Consumer Access

Not all earned wage access works the same way. The two dominant models differ in who funds the advance, how repayment happens, and how much employer involvement is actually required.

Employer Sponsored Model

In this model, the employer partners directly with an EWA provider, giving employees access to a benefit built into the company's existing payroll system. Because the provider works from verified hours and pay rates, the amount available is accurate, not estimated. Most employer sponsored programs are free or low cost to the business, and many offer employees fee-free options for standard transfer speeds.

Direct To Consumer Model

Here, the employee downloads an app and connects it directly to their bank account, with no employer involvement at all. The provider estimates earnings based on deposit history and patterns, rather than actual verified payroll data. Because there's no employer partnership backing the numbers, this model tends to carry more fees, subscriptions, or tip-based charges, and the accuracy of what's "available" depends entirely on how well the app reads irregular deposit patterns.

Payroll Integration

Employer sponsored access requires a real connection between the provider and the company's payroll or time and attendance tracking software, which is what makes the calculations reliable. Direct to consumer providers skip this step entirely, relying on bank transaction history instead. This is the core technical difference between the two models, and it's why employer-sponsored programs tend to be more precise.

Payment Responsibility

With employer sponsored access, repayment happens automatically through payroll, deducted before the employee ever sees their remaining paycheck. With direct-to-consumer access, the provider debits the employee's bank account directly on or after payday, independent of the employer's payroll cycle entirely.

User Experience Differences

Employer sponsored apps typically feel more seamless, showing a live, accurate earned balance tied to actual hours, especially when they sit on top of robust payroll software platforms. Direct to consumer apps often show estimated available amounts, which can be less precise and occasionally lead to confusion if bank deposits are irregular or inconsistent from one pay period to the next.

Feature | Employer Sponsored | Direct To Consumer |

|---|---|---|

Who Funds The Advance | EWA provider, via employer agreement | EWA provider directly |

Repayment Method | Automatic payroll deduction | Bank account debit on payday |

Employer Involvement | Requires integration and setup | None required |

Data Used | Verified payroll and hours worked | Estimated from bank deposit history |

Typical Fees | Often free or low flat fee | Fees, subscriptions, or tips common |

Earned Wage Access Vs Payday Loans And Cash Advance Apps

When medical bills or car repairs show up before a scheduled payday, employees usually turn to one of three options. Understanding how earned wage access works compared to payday loans and cash advance apps makes it clear why one option consistently costs less.

Source Of The Money

This is the core difference. Earned wage access lets employees withdraw earned wages they've already worked for, tied directly to the employer's payroll through real payroll integration. Payday loans and cash advance apps work differently entirely, they're a form of borrowing money against future income, not access to money already earned. One draws from a paycheck already owed; the other creates a debt that didn't exist before.

Cost And Fees

Fee structures vary sharply across all three. Earned wage access typically charges small transfer fees for instant funding, often with a free option for standard delivery. Payday loans charge interest, sometimes with APRs exceeding 300%, while cash advance apps layer in subscription costs, expedited fees, and optional tips. Since EWA involves accessing your own earnings rather than borrowed funds, the cost structure stays far lower across nearly every comparison.

Repayment Process

Earned wage access repays itself automatically, deducted quietly from the paycheck on the scheduled payday, folded into standard payroll processes with zero action from the employee. Payday loans require a separate repayment, often due in full within two weeks, creating pressure if funds are tight. Cash advance apps typically debit a bank account directly, sometimes causing overdrafts if timing doesn't line up with other bills.

Credit Score And Financial Risk

Since earned pay isn't a loan, there's no credit check involved and no risk to a credit score, regardless of repayment timing. Payday loans can involve credit reporting and, if unpaid, collections activity that damages credit in the long term. Cash advance apps sit somewhere in between, generally no credit impact, but repeated use can quietly become a costly habit that outweighs its convenience.

Processing Time And Fund Availability

All three options move fast, but the details differ. Earned wage access usually delivers earned wages early, within minutes, for a fee, or one to three days for free. Payday loans and cash advance apps often promise similarly quick funding, but the tradeoff shows up later in cost, not speed. For employers thinking about employee retention, offering a faster and cheaper way to access earned wages early tends to build far more goodwill than employees relying on payday lenders out of necessity.

Feature | Earned Wage Access | Payday Loans | Cash Advance Apps |

|---|---|---|---|

Source Of Money | Employee's own earned wages | Borrowed against future income | Borrowed against future income |

Typical Cost | Small flat transfer fee, often free option | Interest, APR often 300%+ | Subscription, expedited fees, tips |

Repayment | Automatic payroll deduction | Full repayment due, often in two weeks | Bank account debit on payday |

Credit Check Required | No | Sometimes | No |

Credit Score Impact | None | Possible, including collections risk | Minimal, but repeat use adds cost |

Fund Availability | Minutes for a fee, 1-3 days free | Same day to next day | Minutes to same day |

Benefits Of Offering Earned Wage Access

The advantages extend well beyond convenience. For both the business and its workforce, offering earned wage access changes real outcomes around hiring, retention, stress, and cost, without adding operational burden to the employer.

Reduced Payday Lender Reliance

When employees can access unpaid wages directly through their employer, the pull toward predatory financial services drops sharply. Instead of taking on high-interest debt to bridge a gap before the next payday, workers get instant pay through a benefit tied to money they've already earned. This shift matters most for employees without access to traditional credit, since early pay options don't touch credit scores or require any qualification process at all.

Stronger Hourly And Shift Hiring

Hourly and shift-based roles see the highest demand for flexible pay options, and it shows in hiring results, particularly when combined with broader workforce management software that coordinates schedules, attendance, and pay. Candidates comparing job offers increasingly ask about early pay availability upfront, treating it as a real differentiator rather than a bonus. Employers offering earned wage access often report faster applicant response rates and stronger acceptance rates in competitive labor markets, particularly in retail, hospitality, and logistics, where turnover runs high, and where modern payroll software for startups and growing teams already underpins hiring and pay.

Retention Gains From EWA

Employee satisfaction tends to rise when workers feel more control over the timing of their own pay. Waiting two weeks for money already earned creates quiet resentment that builds over time, especially for employees living paycheck to paycheck. Offering this benefit gives employees one less reason to look elsewhere, and companies that roll it out often see measurable improvement in retention within the first few months, particularly among frontline and hourly staff.

Lower Workplace Financial Stress

Financial stress doesn't stay contained to personal time, it follows employees into their shifts and affects focus, morale, and performance. Giving workers a way to access wages before their next paycheck reduces that background pressure directly, especially when it sits inside broader HR management software that supports financial wellness features. This is a core part of broader financial wellness efforts many employers now prioritize, recognizing that a financially stable workforce is simply a more engaged one.

Zero Impact On Employer Cash Flow

For employers hesitant about cost, this is the detail that changes the conversation, especially once they understand typical HR software pricing and how EWA can ride on top of existing tools. The earned wage access provider funds the advance, not the company, so there's no disruption to existing cash flow or payroll budgeting. Employees typically cover any transaction fee themselves when they choose instant transfer options, while standard delivery windows often remain free, fitting neatly into most HR software billing models. Employers essentially unlock all of these benefits by enabling the integration, not by taking on new financial risk.

Risks And Regulatory Questions Employers Should Know

Earned wage access isn't risk-free just because it isn't a loan. Before rolling it out, employers should understand a few real concerns, both for employees using the benefit and for the business offering it.

Repeat Usage And Debt Masking

Occasional use covers a genuine emergency, but frequent EWA advances can quietly mask a deeper budgeting problem. When someone taps their earned income week after week, it often means regular expenses are outpacing regular pay, not that emergencies keep happening. This pattern can also chip away at savings goals, since every early withdrawal shrinks what's left on an employee's paycheck once payday actually arrives. Employers offering this benefit should pair it with basic financial education, not just access.

Rising And Compounding Fees

While employer sponsored EWA tends to stay cheap, direct to consumer apps built around subscriptions, tips, and expedited transfer fees can add up fast for frequent users. A worker relying on these apps every pay period may end up paying more over a year than they'd expect, especially compared to programs built directly into employer payroll systems. This is one reason employer-sponsored access, with clear flat fees and no compounding cost, tends to serve employees better in the long term.

Federal Guidance Reversals

Regulatory clarity has been anything but stable. The CFPB issued a 2020 opinion treating compliant EWA as separate from credit, then proposed a 2024 rule pointing in the opposite direction, before reversing course again in a later opinion. For employers, this back-and-forth means today's compliant program could face new scrutiny tomorrow, making it worth choosing a provider who actively tracks federal guidance rather than assuming today's rules are permanent.

State By State Legal Patchwork

There's no single national standard right now. Some states have passed laws confirming EWA advances aren't loans, exempting them from usury and interest rules entirely. Others classify them closer to credit, layering on licensing and disclosure requirements. A handful of states still have active legislation sitting undecided. Employers operating across multiple states need providers who can navigate this patchwork and often rely on payroll compliance software to avoid triggering issues in one location while staying fine in another.

Payroll Tax Timing Ambiguity

This one rarely gets discussed, but it's genuinely unresolved. When an employee receives income directly through an early EWA advance, does that count as the actual payment date for withholding and tax deposit purposes, or does the original scheduled payday still apply? Payroll teams need clear answers here, since getting this wrong creates real compliance risk, which is why many lean on payroll automation software that bakes tax rules and deposit schedules into the system. Employers offering EWA without credit checks or new debt still need payroll systems built to handle this timing question correctly, which is exactly the kind of detail worth confirming with a provider before launch, not after.

Is Earned Wage Access Right For Your Business

The honest answer depends on your workforce and your risk tolerance. If your team includes hourly or shift-based employees living close to paycheck to paycheck, offering access to wages earned before payday can genuinely help, without interest charges or the debt cycle tied to short term loans, especially when layered onto simple payroll software for small businesses.

Just go in informed. Regulatory scrutiny is real, some states now have licensing requirements, and coverage from outlets like the New York Times has highlighted providers relying on optional tips or voluntary tips instead of transparent fees, sometimes amounting to high fees in disguise. Choose a provider with clear pricing, and this benefit can pay off without the hidden costs, particularly if you're also planning to move payroll from Excel to software to tighten controls overall.

FAQs

Is Earned Wage Access A Loan?

No. Earned wage access gives employees a portion of wages they've already earned, not borrowed money. There's no interest, no credit check, and no debt created, since the amount advanced simply gets deducted from the employee's paycheck on the next scheduled payday. Regulators have generally treated it as distinct from credit, though this classification is still evolving state by state.

How Much Can Employees Access Early?

This depends entirely on the provider and employer settings. Most programs cap early access somewhere between 50% and 100% of wages already earned in the current pay period, calculated against actual hours worked, not projected future pay, which makes clean employee payroll records even more important. Employers can often adjust these limits based on company policy and workforce needs.

Does Offering It Cost Employers Anything?

Typically, very little to nothing. The EWA provider funds the early payments, not the employer, so company cash flow stays untouched. Most employers pay a setup or integration fee at most, while any transaction costs are usually covered by the employee choosing instant transfer, with standard delivery often free, and the broader move from spreadsheets to HR and payroll software often unlocks these integrations.

Can Employees Misuse Earned Wage Access?

It's possible. Using it occasionally for real emergencies is exactly what it's designed for, but frequent, repeated use can mask a bigger budgeting issue rather than solve it. Some employees may also underestimate how much smaller their next paycheck will feel after repeated early withdrawals, which is why pairing access with basic financial guidance helps.

Is It Available Outside The US?

Yes. Earned wage access has expanded well beyond the US, including the UK, where it's sometimes referred to as an Employer Salary Advance Scheme, and often ties into cloud-based attendance management systems for small businesses. Adoption and regulation vary by country, with some regions further along in building formal oversight than others, so availability and terms depend heavily on local providers and labor laws, as well as the timesheet and employee timesheet apps employers already use.